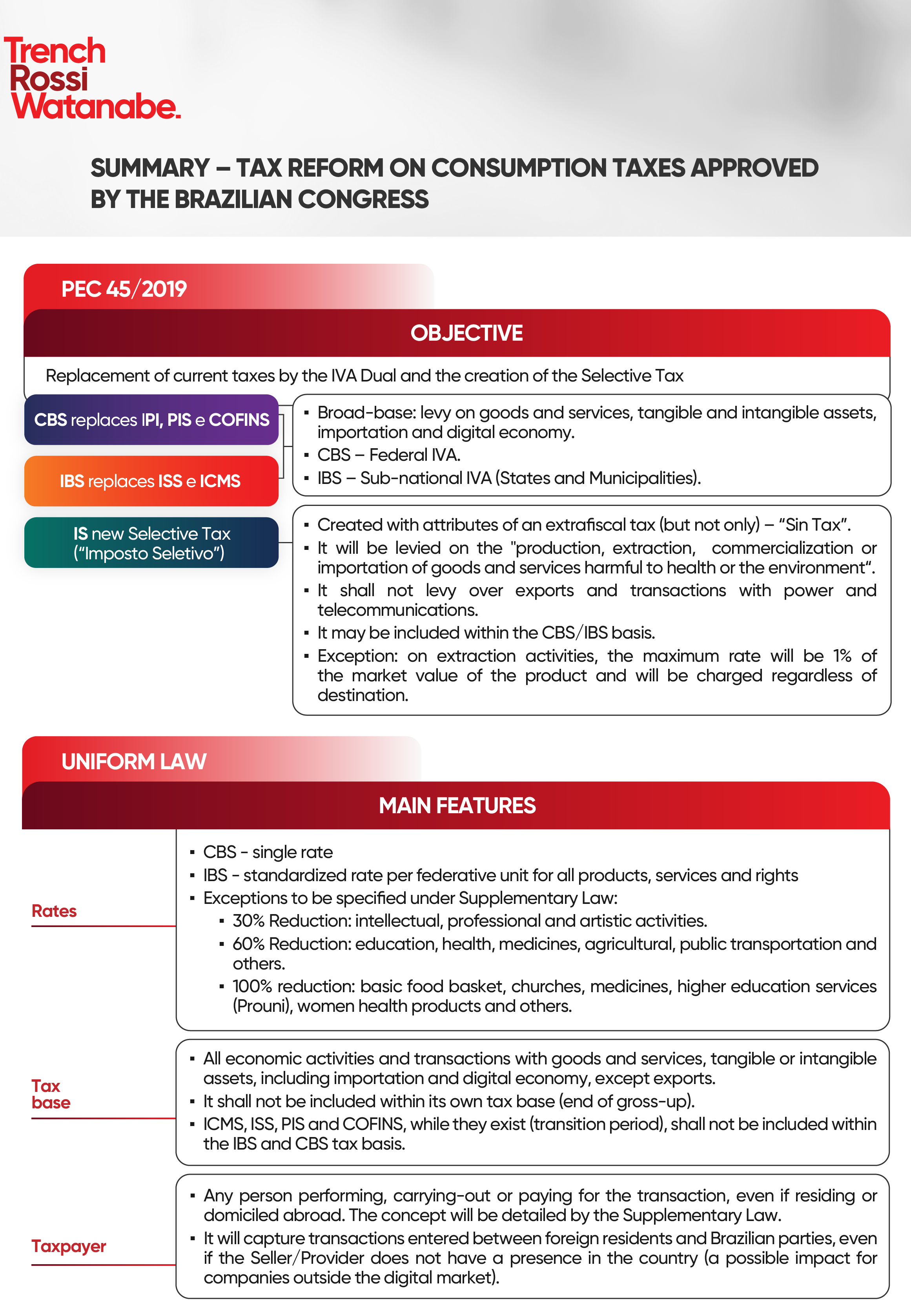

Cemig and Tax Reform: Challenges for Funding and Local Revenue

As Brazil undergoes major tax changes, industry leader Cemig is evaluating its cultural investment strategy, while municipalities in Mato Grosso prepare for new tax administration rules to protect local revenues during this critical economic transition.

Read it in Short

QUICK OVERVIEW

Cemig invested R$ 99 million in 114 cultural and sports projects in 2026.

Legislators and Cemig are discussing how Tax Reform restricts current sponsorship models.

Mato Grosso municipalities are conducting training to adapt to new IBS tax regulations.

Both private and public sectors are focusing on ensuring revenue stability during the transition.

As Brazil navigates significant shifts in its financial landscape, the energy company Cemig is actively addressing how the ongoing Tax Reform affects corporate funding for cultural and sports initiatives. During a recent legislative hearing at the Legislative Assembly of Minas Gerais (ALMG), representatives emphasized that while the company remains a major investor—allocating R$ 99 million across 114 projects this year—there are persistent challenges in distributing these funds effectively to interior regions.

Why Tax Reform Impacts Public and Private Investment

The intersection of national tax policy and regional economic management has become a focal point for organizations across the country. In a parallel development within Mato Grosso, the Mato Grosso Municipal Association (AMM) is hosting a strategic seminar to discuss the implications of the Tax Reform on local municipal revenue. This event gathers experts from the National Confederation of Municipalities (CNM) and the State Secretariat of Finance (Sefaz/MT) to evaluate how new rules will reshape local tax collection, including the ISSQN and ICMS quotas.

For large corporations like Cemig, the Tax Reform necessitates rigorous study to ensure that sponsorship and social investment models remain viable under a modernized tax framework. The primary goal is to bridge the gap in regional development, ensuring that financial support for sports and arts is not concentrated in metropolitan hubs but reaches underserved communities.

How Municipalities Are Adapting to New Tax Rules

The transition to the new tax system requires comprehensive administrative adjustments. Municipalities are focusing on:

- Adapting to new calculation methods for IBS (Goods and Services Tax) indices.

- Implementing stricter fiscal controls to maintain revenue stability.

- Developing long-term strategies for sustainable public spending during the transition phase.

- Aligning accounting practices with federal requirements to secure municipal shares of tax revenue.

As these sectors evolve, stakeholders are increasingly focused on how to maintain public service quality while navigating the complexities of the new tax landscape. The combined efforts of public entities and private sector leaders indicate a broader national effort to standardize tax compliance while mitigating the risks of revenue loss during this pivotal period of economic reform.

Frequently Asked Questions

What are the main concerns regarding Tax Reform for companies like Cemig?

The primary concern involves maintaining the ability to sponsor cultural and sports projects while adjusting to new tax laws that could restrict traditional funding mechanisms.

How are municipalities in Mato Grosso preparing for the new tax system?

Municipalities are participating in specialized training seminars to understand the new IBS and ISSQN rules, ensuring they can optimize tax collection and comply with upcoming federal mandates.

Source Statement

This briefing is distilled from the original source to provide you with clear, structured insights for immediate value.

Read the full source story: Cemig Debates Cultural Funding Impacts Amidst Ongoing Tax Reform

Read the full source story: Cemig Debates Cultural Funding Impacts Amidst Ongoing Tax Reform