Secure Rs 50,000 Monthly Pension with Early Savings

Securing a monthly pension of Rs 50,000 in retirement requires early investment strategies and robust financial planning, leveraging mutual funds and SWPs to combat inflation.

Highlights

- •Early investment is crucial for building wealth over time through compounding

- •Equity mutual funds offer long-term returns that align with inflation rates

- •Public Provident Fund (PPF) and National Pension Scheme (NPS) ensure capital protection during retirement

- •Systematic Withdrawal Plan (SWP) provides consistent monthly income in retirement

In today's fast-paced world, securing a financially comfortable future is a top concern for many. The idea of relying solely on savings or children during retirement can be daunting. If you're in your 20s and think planning for retirement should wait until the 40s, think again. Experts emphasize the power of compounding, suggesting that starting investment early can significantly ease financial burdens later.

According to financial advisors, beginning investments at a young age requires less effort over time to build substantial wealth compared to waiting until mid-career. This principle is aptly called 'the power of compounding,' where your initial capital not only accrues interest but also earns returns on the generated interest. This phenomenon serves as a robust financial cushion for the future.

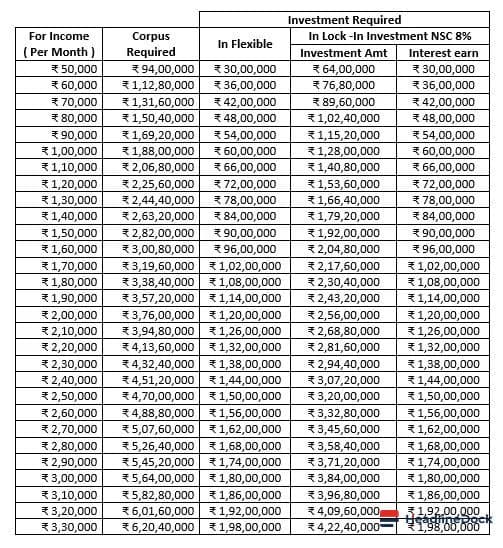

Strategy for Secure Pension

To secure a monthly pension of Rs 50,000 over the next two and a half decades post-retirement, it's crucial to strategically allocate your funds. While fixed deposits (FDs) or gold are popular choices in India due to their perceived stability, they may significantly lose value with rising inflation.

Equity mutual funds offer substantial long-term returns of 12% to 15%, which help keep pace with the inflation rate. Conversely, tools like Public Provident Fund (PPF) and National Pension Scheme (NPS) ensure your capital is well protected. A Systematic Withdrawal Plan (SWP) allows you to withdraw a consistent amount from these investments monthly post-retirement.

The idea of SWP involves setting aside a lump sum upon retirement, which is then withdrawn systematically over time. This method ensures steady income in later years while maintaining the capital for growth, providing both security and flexibility.

For instance, if you invest Rs 10 lakhs at a 12% annual return rate using an SWP, it can provide Rs 50,000 monthly starting post-retirement. This financial strategy not only helps manage cash flow but also harnesses the power of compound interest effectively.